The recent outbreak of the Wuhan Coronavirus is a topic that is at the forefront of all investors’ minds, particularly since information out of China is spotty and the numbers that are supplied by the Chinese government need to be met with high scrutiny. Many would wonder how the world’s second largest economy seemingly grinding to a halt would not cause a market sell off. The market reaction thus far has been relatively muted for several reasons:

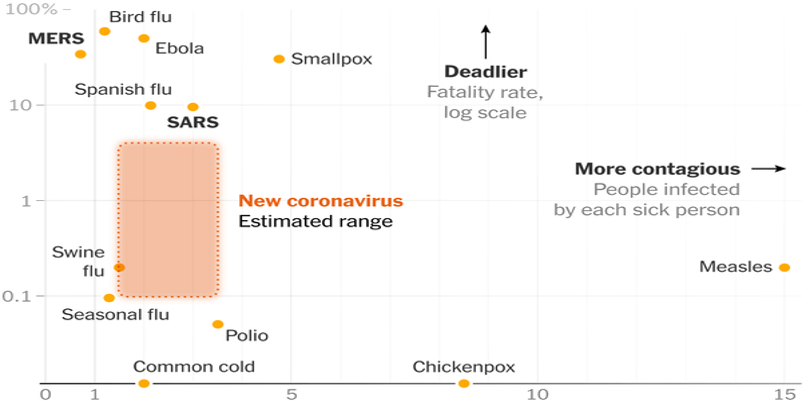

The first reason is the derivative effects of the virus that the market is currently pricing in. The market is confident that China will be able to relatively contain the virus before it becomes a full-on Global Pandemic. From what we know now, the mortality rate from Coronavirus is relatively low. Figure 1, located below, plots the Coronavirus mortality statistics against similar outbreaks. As this is being written, only two deaths have been confirmed due to the virus outside of China. In the last few days several Chinese factories have announced that they are resuming operation and workers are returning to facilities. A minor detail that may soften the impact to U.S. companies’ inventories is that the virus outbreak has taken place over the Chinese New Year which is a period where factory output is predicted to be depressed. What the market is then pricing in is that once economic production resumes, economies will undergo a sharp increase in activity to make up for lost production due to the virus. Think of this as a “V-Shape” bounce on a graph.

Another derivative effect that the market is looking forward at is Central Bank stimulus. Just in the last few days the Peoples Bank of China injected 900 billion yuan (about 129 billion U.S. dollars) into the Chinese financial system. U.S. investors are predicting that the impact from the virus, and subsequent impact to GDP, will cause the Federal Reserve to continue to be accommodative via their own repurchase operations and possibly another rate cut. Many companies that have reported numbers in the last month have also given wide forward-guidance due to uncertainty from their supply chain status. This should dampen the shock that investors will get if subsequent numbers are materially impacted from their production or inventory drawdown.

Figure 1 | Source: New York Times

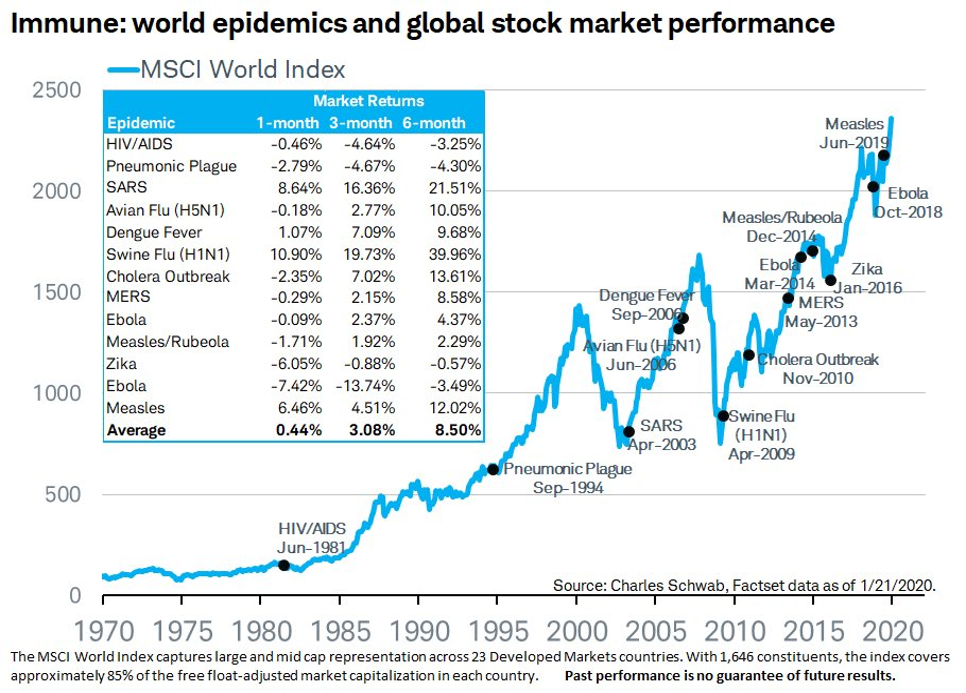

The second reason is the historical precedent that we have to try to judge the effects of a virus outbreak similar to what we have now on markets. Although no two situations are completely alike, the Coronavirus is not the first time the market has had to digest a similar risk. The Ebola outbreak in 2014 is perhaps the most recent outbreak of this scale but the most similar in terms of geography is the SARS outbreak in 2003. Both were followed by positive three and six month equity returns as measured by the MSCI World Index. Today China is a much larger chunk of global GDP than it was in 2003 which is a factor that must be considered. Even so, investors are still confident that this storm will be weathered. Investors also think that the repatriation of American production that has taken place in the past few years due to the trade war, such as Apple’s factory investments in the U.S., will dampen the effect that a supply chain disruption stemming from China will have on today's markets. Figure 2 plots the MSCI World Index since 1970 overlaid with world epidemics and subsequent market returns. As you can see the effects that these events have on the stock market is incredibly difficult to predict. The worst thing an investor can do is panic and unload their shares at the wrong time and then try to jump back in at a later date.

Figure 2 | Source: Charles Schwab & Co., Inc.

We build our portfolios with the intention that we will have an economic calamity sometime in the near future. The average age of a company in our portfolios is over 80 years old. Our companies have not only weathered events worse than the Coronavirus but have taken market share from their competitors during periods of strain and come out stronger on the other side. Our dividend bias creates cash flow for clients while we wait for our companies to maneuver through transition periods. On top of historical durability, our companies have strong balance sheets that have been heavily scrutinized. Many of our companies actually hold net cash on their balance sheet meaning they could pay off all of their outstanding debt today with cash on hand if they wanted to. When you pair these large cash reserves with good capital allocating management teams a market sell-off is welcomed by these companies. It gives them the chance to deploy this cash into profitable expenditures at attractive prices.

The graphic below provided by Morningstar shows the dynamic between market sell offs, rebounds, and the reason timing the market is so difficult. In the short term markets can be spooked by events such as a global virus outbreak, but in the long term it is just a blip on the radar and markets continue to rise because our economic foundation is strong.

Figure 3 | Source: Morningstar

Conclusion

We continue to monitor the situation in China closely. As always, if any clients have any questions or would like further insights related to their investment strategy please feel free to reach out to us.

Disclaimer: The information contained in this commentary has been compiled by Covington Investment Advisors, Inc. from sources believed to be reliable, but no representation or warranty, express or implied, is made by Covington Investment Advisors, Inc., its affiliates or any other person as to its accuracy, completeness or correctness.

Under no circumstance is the information contained within this correspondence to be used or considered as an offer to buy or sell or a solicitation of an offer to buy or sell any particular security. Nothing in this correspondence constitutes legal, accounting, or tax advice or individually tailored investment advice, or research. This material is prepared for general circulation to clients and does not have regard to the particular circumstances or needs of any specific person who may read it. The recipient of this correspondence must make his or her own independent investment decisions regarding any securities or financial instruments mentioned herein. Past performance is not indicative of future results.

To the full extent permitted by law neither Covington Investment Advisors, Inc. nor any of its affiliates, nor any other person, accepts any liability whatsoever for any direct, indirect or consequential loss arising from any use of this market commentary or the information contained herein. This correspondence may not be reproduced, forwarded or copied by any means without the prior consent of Covington Investment Advisors, Inc.

Investors should review this correspondence knowing that any comments and opinions made in this correspondence are subject to change and positions held by the authors may be sold.