Life Cycle of a Virus Pandemic (3/27/2020)

Now is the time to look forward and stick to a plan of action. Virus pandemics have a lifecycle that they go through and just like every life cycle they are not exact but can be useful as a timing tool. This framework is important for us as we navigate this volatility and make tactical investment decisions. Our timing will never be exact but what is important is that we are not basing our investment decisions on panic rather than sticking to realities and our core investment philosophy.

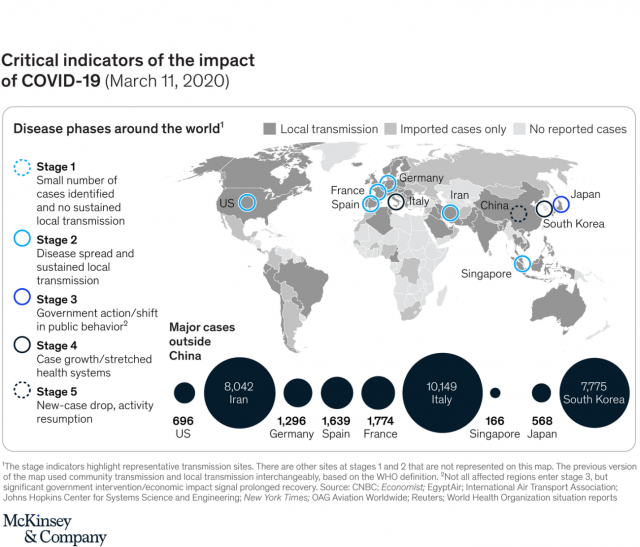

The current coronavirus cycle is broken down into 5 stages. Right now, we are crossing over from stage 2 to 3. After the initial spotty cases across the country now we are seeing person to person transmission and the number of total cases to expand dramatically. Our transmission rates have been on par with other countries, but our mortality rate is significantly lower, and we think that will continue to be the case on account of our more robust health care system and better hygiene standards.

As we transition into the later stage, we have confidence that our healthcare system can handle the shock that the virus is levying. One of the reasons why the Virus decimated China, particularly in the Hubei providence, is because their health care system was not prepared to handle it.

Finding the Bottom

For a trough to occur in equities there are several key factors that we would still like to see before we felt confident a bottom in equities was occurring:

- A peak in daily infection rates.

- A trough in global manufacturing indexes.

- Coordinated monetary, and fiscal stimulation by governments and institutions around the globe.

- A market correction indicating that equities have re-rated to price in sufficient uncertainty.

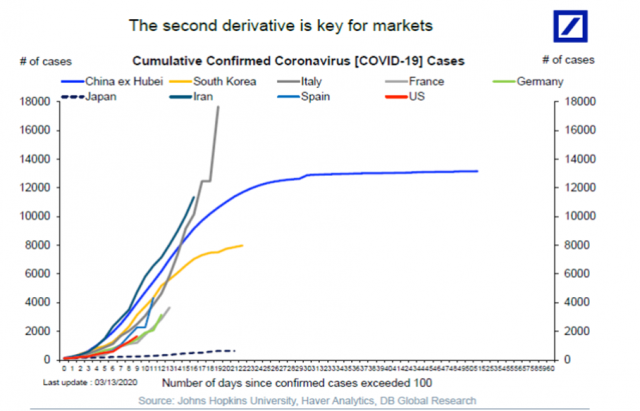

A Peak in Global Infection Rates

This is the most important factor for sensing a market bottom but also the most difficult to predict because of the uncertain nature of viruses. Using available data and models we can estimate the timeframe that it takes for a country to reach its peak infection rate and then flatten out.

Many governments around the world believe the virus will peak in June or July but using China as an example we believe that peak could occur even earlier as long as countries take the necessary precautions to curb the spread of the virus. Every country has different circumstances. Italy for example has not been effective at stopping the virus and an aging population has made the mortality rate especially high. On the other hand, South Korea has shown the ability to stem the spread of the virus in an outstandingly quick timeframe through extensive testing and quarantining measures. During the SARS crisis the buying opportunity was one week after this peak in new infections occurred.

Trough in Global Manufacturing Indexes

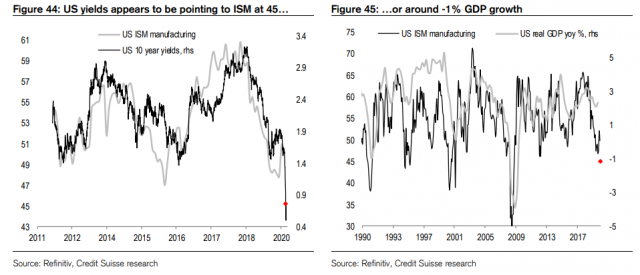

Manufacturing indexes give investors an insight into what economic activity is and they are used as a gauge for business sentiment. These indexes are one of the most common forms of “Leading Indicators” because they can give hints at what might happen in the future rather than looking into the past. To be confident that equities are troughed we would first like to see that manufacturing indexes have bottomed out as well. Global PMI indexes can give us hints for what Global GDP prints come in as and when they might bottom. This indicator has not yet bottomed and is implying global GDP growth of 1% for 2020.

For the U.S. Specifically these indicators are pointing to -1% GDP growth for 2020.

Coordinated Stimulus from Institutions Around the World

Low interest rates, expanding central bank balance sheets, and stimulative fiscal policy will not stop the spread of the virus. But what it will do is ensure that liquidity does not dry up and financial institutions can continue to function properly, as well as provide extra support for when the virus panic clears, and the economy needs to pick up slack quickly.

Over the weekend the Federal reserve announced a sweeping stimulus package including cutting interest rates to zero and expanding their treasury purchase program to $700 Billion dollars. Along with these short-term treasury purchases the Fed will continue buying mortgage backed securities.

Along with this monetary stimulus the Trump administration has unveiled a more comprehensive testing program and is working with congressional leadership to pass a large fiscal package which is rumored to include tax cuts.

These policies are also being enacted by other countries around the world creating an attractive environment for a quick rebound from the economic damage caused by the virus.

Rerating in Equities

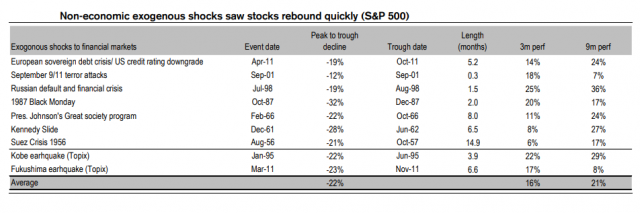

For noneconomic shocks the market reacts quickly both on the selloff as well as the rebound. There comes a point where averages can be used as loose templates for comparing the current 28% drawdown from peak to historical sell offs. The long-term impact from the virus is not known and certainly has the possibility to cause lasting financial damage. But eventually capitulation will be reached, and the market will bottom itself out.

Conclusion

We will continue to monitor this Virus outbreak closely as we navigate this crisis. Although we will not time the bottom perfectly it is important to consider the data that we have available so that we can deploy your capital effectively while providing the least amount of risk. For those accounts with excess cash we will be proceeding with the buyside in a prudent manner. We will use this volatility to our advantage to dollar cost average into our positions. It is not a one-time event but a process. If you have reassessed your situation or have objections to the remainder of your cash being invested please notify us immediately.

For those accounts fully invested we reiterate that times like these are why we recommend keeping 6-12 months of emergency funding in a liquid account. This way we can sail through these periods of strain without being forced to sell significant positions while the market is being irrational. If any of you would like further guidance please feel free to reach out to us.

Sincerely,

Patrick Wallace

Disclaimer: The information contained in this commentary has been compiled by Covington Investment Advisors, Inc. from sources believed to be reliable, but no representation or warranty, express or implied, is made by Covington Investment Advisors, Inc., its affiliates or any other person as to its accuracy, completeness or correctness.

Under no circumstance is the information contained within this correspondence to be used or considered as an offer to buy or sell or a solicitation of an offer to buy or sell any particular security. Nothing in this correspondence constitutes legal, accounting, or tax advice or individually tailored investment advice, or research. This material is prepared for general circulation to clients, and does not have regard to the particular circumstances or needs of any specific person who may read it. The recipient of this correspondence must make his or her own independent investment decisions regarding any securities or financial instruments mentioned herein. Past performance is not indicative of future results.

To the full extent permitted by law neither Covington Investment Advisors, Inc. nor any of its affiliates, nor any other person, accepts any liability whatsoever for any direct, indirect or consequential loss arising from any use of this market commentary or the information contained herein. This correspondence may not be reproduced, forwarded or copied by any means without the prior consent of Covington Investment Advisors, Inc.

Investors should review this correspondence knowing that any comments and opinions made in this correspondence are subject to change and positions held by the authors may be sold.

)