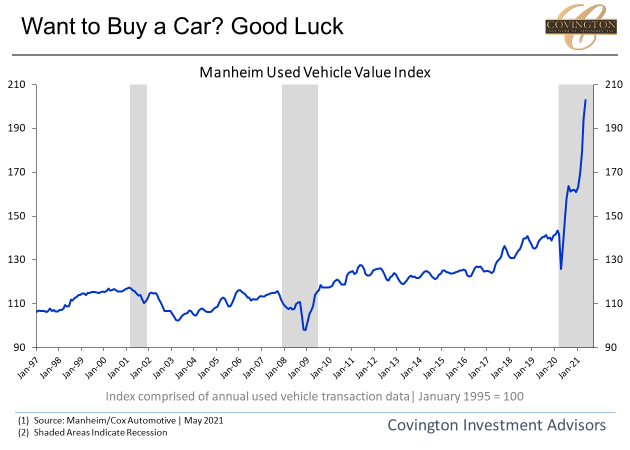

If you have tried to buy something like a car or washing machine lately you probably know firsthand about the challenges of lean inventories & price pressures and are not surprised by the surge in inflation readings that have filled media headlines. Inflation is not only salient because it affects businesses/consumers but also because of its effect on interest rates, and therefore asset prices. But inflation is also an economic phenomenon in the sense that it is maybe the most discussed financial topic but also the least understood by forecasters when applied to real world developed economies. In our January 2021 Economic Outlook we highlighted runaway inflation as a key risk for the economy in the New Year, but also why the long-term picture is not as clear.

The view by the Federal Reserve and one which we largely share is that inflation will be transitory driven by supply chain bottlenecks … but transitory can feel like a long time. When you essentially turn off & turn back on the World economy it will take some time to find balances. Just like the economic data stunned us during the lockdown, the same is happening now with reopening. Very aggressive fiscal and monetary policy has led to a burst in reopening and many parts of the supply-side of the economy are simply trying to keep up. The hope is that shortages will start to ease as supply catches up to demand, but this won't happen overnight. We think we are at least several quarters away from the economy feeling more balanced. If we had to step out and make a forecast on inflation it would be one of phases: 1.) temporary burst in inflation as shortages from shutdowns drive up goods prices and reopening supports services pricing 2.) softening of inflation as economic growth rate peaks in second half of year and supply chains relieve themselves of bottlenecks 3.) labor market pressures push core inflation modestly higher at a faster pace than pre-covid due to wage inflation...

..

..

..

..

..

..

..

..

..

..