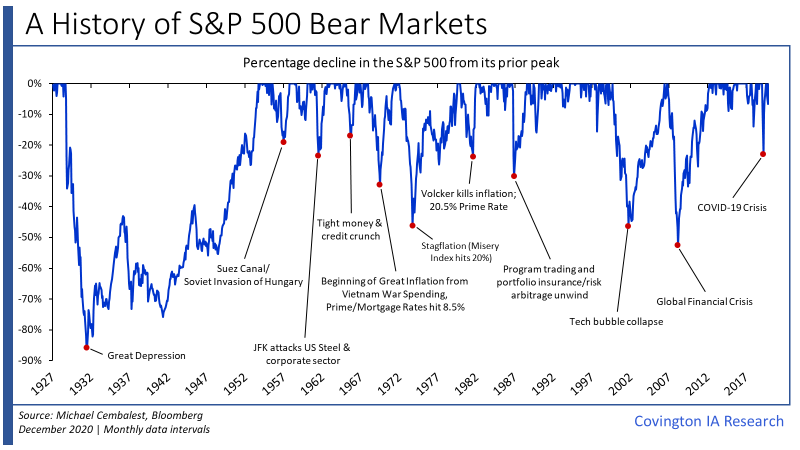

Market drawdowns and Bear Markets are a reality when it comes to investing in the equity markets. Part of the reason equity holders receive a higher long-term return over ‘safer’ investments such as bonds is that they take on additional risk and the likelihood that their investment will be negative over stretches of time. Of course no investor wants to experience their investment losing money but this year illustrates perfectly why sticking to a plan and staying invested while owning proven enterprises with strong balance sheets is the prudent approach. This fact of investing is nothing new but the rise of social media and the competitiveness for media headlines since 2010 have given way to a flood of negative market calls which naturally appeals to human negativity bias and our survivorship instincts. This appeal strategy has worked in part because the flood of calls followed two of the deepest bear markets since the great depression: The Tech Bubble & Global Financial Crisis.

Of course, just as there is inherent risk with being invested in the equity markets, there is also risk in not being invested.This is through the opportunity cost of trying to time the markets by jumping in and out of investments or dramatically drifting away from asset allocations due to “Armageddonist” media headlines. For example, $1 shifted from equities to bonds in 2014 in response to mega-bearish commentary would have underperformed equities by roughly 40% as the S&P 500, propelled more by earnings growth than by multiple expansion, rolled on...

..

..

..

..

..

..

..

..

..

..

..

..

..

..